If you asked me about whole life insurance a few months ago, I wouldn’t even know where to begin.

Whole life insurance? Doesn’t that mean your kids will get money after you die? Most people think that’s only what it does, but the truth is that’s only a fraction of it.

Whole life insurance functions like most insurance, in terms of paying a premium monthly, quarterly, or annually, but the thing that makes it vastly different is that the money you pay on your plan goes towards your death benefit! Did you know that you can access your death benefit at any time, and any age? That money is also tax free!

Whole life insurance functions like most insurance, in terms of paying a premium monthly, quarterly, or annually, but the thing that makes it vastly different is that the money you pay on your plan goes towards your death benefit! Did you know that you can access your death benefit at any time, and any age? That money is also tax free!

When you purchase a whole life policy the insurance company invests your premium in the chance to add to your cash value. This is called a dividend, and it comes as no cost to you. At the time you sign up for the policy you’re given a set amount that your death benefit can mature to, so even if the carrier doesn’t profit from investing, you are always guaranteed that specific amount.

Not only does a whole life insurance plan have the potential to make you money, it is certified insured for the rest of your life. For a small cost, you can  add an “accelerated death benefit rider” to your plan. If you are diagnosed with a chronic or terminal illness, the insurance carrier will give you more than 50% of your death benefit.

add an “accelerated death benefit rider” to your plan. If you are diagnosed with a chronic or terminal illness, the insurance carrier will give you more than 50% of your death benefit.

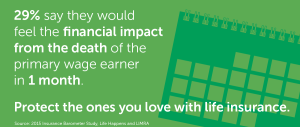

What would you do with the money your whole life insurance builds? With access to your benefit anytime you need without penalty, you could purchase something you’ve always wanted. Even if you find yourself in a tough spot in life, you can use it to help pay for your groceries and monthly bills. The money is yours to do with however you please.

Speak to an adviser to make sure your policy is properly designed with high cash value percentages from year one. You get insurance for your car, home, and electronics, why not get some for yourself? Learn how to maximize what you get out of a whole life insurance policy.